Energy Abundance in the AI Era

Building the power backbone to sustain the AI revolution.

April 22, 2026

AI may be the most transformative technology of our lifetime, but its scale is defined by electrons. Every new model, inference, and data center expansion requires energy.

A few months ago, we highlighted an escalating challenge: AI’s infrastructure surge is pushing the U.S. power system to its limits. Data centers and AI workloads are now consuming electricity at manufacturing-scale levels in some regions, while constraints on interconnection, transmission, and grid capacity threaten to slow future infrastructure buildouts. The impact reaches far beyond the grid itself — rising power demand is affecting energy prices and straining water supplies as new data centers compete with existing energy and infrastructure needs.

The inextricable link between compute and power means that for AI to scale, our energy supply chain must undergo a fundamental evolution. At Salesforce Ventures, we view AI’s energy requirements as both an urgent issue and an unprecedented opportunity. AI represents a unique paradox: it’s a significant new driver of power demand, yet it’s also the most powerful tool we have to optimize, manage, and ultimately unlock a new era of energy abundance.

Consequently, Salesforce Ventures is actively investing across the energy + AI value chain. To date, our team has partnered with companies like Base (vertically integrated battery technology enabling a new wave of distributed energy), Crusoe (power diverse, scalable AI data centers), Emerald AI (intelligent power demand flexibility), and Weavegrid (EV charging optimization). These companies, and many more, demonstrate how AI-enabled solutions have the potential to become the backbone of modern energy infrastructure, enabling a wider variety of power sources to integrate with the grid more efficiently.

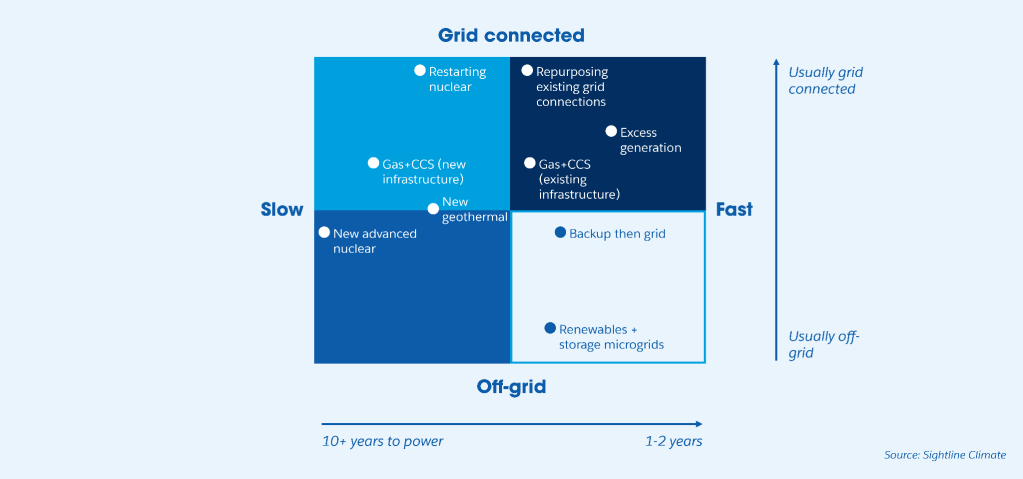

Understanding the energy landscape is central to our investment thesis. The companies building tomorrow’s AI need power solutions that are abundant, affordable, and deployable at speed. This analysis identifies the emerging generation sectors primed to support AI-era demand and highlights the most significant opportunities for innovators. While this first chapter focuses on generation, a following installment will explore the technologies rewriting the energy supply chain. With so much at stake, understanding today’s landscape is crucial to shaping the global future of energy and AI, and making long term financial bets.

The Future of Energy Generation

Fossil fuels remain the backbone of today’s energy system, supplying roughly 80% of U.S. energy and 56% of current data center power globally. Oil and gas companies are thinking about ways to shift their footprint through novel technologies that remove carbon from the atmosphere. In December 2024, ExxonMobil announced plans to build a 1.5+ GW natural gas facility with Carbon Capture and Sequestration (“CCS”) for a data center, designed to remove over 90% of CO₂ emissions.

At Salesforce Ventures, we believe the next chapter requires continued improvements to legacy infrastructure, as well as meaningfully scaling emerging reliable energy sources while modernizing the U.S. grid to carry them. Our analysis will focus primarily on the latter approach.

The path forward centers on five technologies we view as best positioned to meet the AI moment: renewables, batteries, geothermal, nuclear fusion, and nuclear fission. Together, these form the foundation of a resilient energy mix capable of expanding the supply available to data centers, and sustaining AI innovation at the scale the moment demands.

Summary

- Renewables: The most cost-competitive and scalable long-term solution for AI power needs. This sector is driven by dramatic declines in levelized energy costs, rapid modular deployment, and mature supply chains, further enhanced by AI-driven optimization for grid reliability.

- Batteries: A flexible, near-term solution for grid congestion, batteries enable fast deployment and resilience through distributed systems and virtual power plants.

- Geothermal: A reliable, always-on renewable energy source with near-zero emissions and low operating costs, geothermal is gaining momentum through federal and state support, AI-driven subsurface discovery and drilling advances, and increasing investment from enterprises seeking stable, clean power for data centers.

- Fusion: Once purely theoretical, fusion is moving toward commercial viability as investment shifts from physics risk to deployment risk — accelerated by AI-driven solutions in plasma control, simulation, and materials discovery.

- Fission: Small modular reactors offer carbon-free, AI-scale baseload power with lower cost and risk through factory-built standardization, on-site deployment at data centers, advanced passive safety systems, and growing interest from hyperscalers and institutional investors — though regulatory and safety hurdles remain.

Renewables

Renewable energy comes from natural resources that replenish faster than they’re used. Within this category, solar and wind power offer some of the most viable long-term solutions for scaling AI infrastructure driven by a potent combination of economic deflation, rapid strategic deployment, and necessary policy modernization.

Over the last decade, the levelized energy costs for solar and wind have decreased dramatically. Solar energy, in particular, has seen a 90% cost reduction over the last decade, making it one of the most cost-effective energy sources available. On an unsubsidized $/MWh basis, solar and wind remain among the most cost-competitive forms of generation.

Technology improvements and economies of scale account for the majority of the reductions, with over 60% of the decline in total installed cost between 2010 and 2024 stemming from reductions in module and inverter costs. AI-powered predictive generation, grid integration, and energy optimization tools are further enhancing the efficiency and reliability of solar and wind energy.

One of our portfolio companies, Crusoe, offers a powerful example of this innovation. Unlike traditional cloud or data center operators, which start with compute demand and then scramble to secure power, Crusoe begins by securing stranded power assets, including renewable energy sources, and then builds advanced AI compute infrastructure around them. By breaking from grid-bound convention, Crusoe accelerates speed to power, providing a meaningful competitive advantage in time-to-market, operational cost efficiency, and sustainability.

Outside the portfolio, we’re particularly excited by companies tackling renewable energy challenges in creative, non-obvious ways. Exowatt is rethinking how solar integrates with the grid by using the sun’s energy to heat rock-like materials that store thermal energy for up to five days, enabling always-on power for energy-intensive use cases like data centers. At the same time, companies like tem and Crux are modernizing how clean energy is bought and sold — building more efficient, transparent transaction systems that make renewable energy simpler and fairer to access.

We believe solar and wind power are positioned to play a key role in energy innovation over the long term because they solve the core economic, strategic, and corporate challenges presented by the AI boom:

- Declining cost curve: Solar and wind offer continual reductions in manufacturing, installation, and operational costs.

- Scalability and global reach: Being both modular and rapidly expandable, solar and wind enable flexible deployment across diverse geographies.

- Sustainability imperative: Solar and wind enable “clean by design” operations for digital infrastructure and enterprise computing.

- Momentum and ecosystem development: Solar and wind come with mature supply chains, standardized project finance, and improved operational experience.

- Software as an enabler: AI enhances efficiency and reliability through predictive generation and grid optimization.

The cost-reduction trajectory of key renewable energy technologies represents one of the most significant technological achievements in history, and makes renewables an essential ingredient in achieving the long-term, predictable cost structure necessary for competitive AI infrastructure.

Batteries

Batteries convert stored chemical energy into electrical energy to power electronic devices. While renewables (and, as we’ll discuss further down, nuclear) offer a viable path towards energy abundance, they’re also hampered by regulatory hurdles and an aging U.S. power grid, where interconnection times can stretch to decades. Battery power, on the other hand, is decentralized, modular, and more flexible, making it a viable option to meet the immediate demands of the AI data center boom.

An example of the efficacy of battery power comes from our portfolio company, Base. The Base team is using battery hardware, software, and retail electricity services to stabilize the grid and meet energy demand in their home state of Texas. This vertical model gives Base control over costs, improves reliability, and dramatically accelerates deployment. To date, Base has delivered 1.62 years of backup power for its Texas customers, improving grid stability across the state.

Each of Base’s batteries takes less than a day to install, and in aggregate, Base can install enough batteries to reach the same power capacity as a utility-scale battery in only 3-6 months — a fraction of the time required for conventional power plants. By installing batteries directly in customer homes, Base can leverage grid price fluctuations for energy arbitrage, charging batteries from the grid during low-peak times and selling power back to the grid or to the home during high-peak times — thereby improving both reliability and affordability for consumers.

Over the long term, Base aims to build distributed power plants to serve utilities and hyperscalers. For hyperscalers, Base can provide a 100 MW utility-grade power asset in a matter of months, offering a capacity lifeline that alleviates grid congestion, accelerates data center interconnection, and improves homeowner resiliency in the region. On the utility front, they just launched their largest partnership to date with CoServ for 100 MW, and have several utility partnerships already underway.

In this same space, we’ve been impressed by the advancements of companies like Form Energy, which is developing an iron-air battery capable of storing 100 hours of energy cost-effectively, and Antora, whose team has brought to market a thermal battery that stores heat in blocks of solid carbon. Both solutions promise to advance energy reliability and security.

We view battery power as a crucial component in expanding energy capacity and ensuring the grid can scale alongside rising demand. Distributed energy resources are the most viable near-term path to rapidly scaling reliable energy capacity across the U.S.

Broadly, Virtual Power Plants (“VPPs”) could scale to meet an estimated 20% of U.S. peak demand by 2030. Governments are already signalling their support for battery power solutions. Extensive incentive programs exist across the U.S. to motivate homeowners to install batteries. California, New York, Massachusetts, Vermont, Hawaii, and Texas, among others, also have state-wide incentive programs to fund battery storage. The speed and flexibility of battery deployment — particularly compared to the multi-year timelines of traditional infrastructure — make this one of the most pragmatic solutions for bridging the gap between current capacity and AI’s explosive energy demands.

Geothermal

Geothermal is a form of renewable energy that harnesses the thermal energy generated and stored within the earth. This heat originates primarily from the decay of naturally radioactive isotopes in the crust and mantle, supplemented by residual heat from the planet’s formation. While conventional geothermal has been a power source for over 100 years, this generation is largely limited to hotspots in the western and southern U.S., with a handful of smaller projects in Europe. As such, geothermal currently makes up only 1% of global energy. However, next-generation geothermal technology advancements, its near-zero emissions, 24/7 reliability, and low operating costs once online make geothermal a highly promising energy source for AI infrastructure.

The DOE has found that geothermal energy has the potential to produce 60GW of electricity output by 2050, and the government has indicated their support in building out the necessary infrastructure to support geothermal energy production. At the state level, New York, Colorado, and Washington have all passed legislation in recent years focused on expanding access to geothermal energy. Just recently, Cornell University shared that it was drilling for geothermal energy near its campus in Ithaca, New York.

AI is playing a key role in geothermal expansion. Innovations in the fields of subsurface modeling and drilling location targeting, well health and productivity, and refinery production management are all being driven by AI. Companies in this space include Zanskar, Quaise, XGS Energy, and Fervo Energy. Fervo, for example, is pioneering next-generation techniques that borrow fracturing methods from the oil and gas industries to create reservoirs where none exist naturally, effectively unlocking geothermal potential almost anywhere, key to commercial expansion. The company’s 500 MW Cape Station project in Utah, expected to begin delivering power in 2026, marks a critical early step in the commercialization of geothermal energy.

Similar to nuclear and renewables, institutional investors and enterprises are looking to geothermal power to help support the AI data center buildout. Microsoft, Meta, and Google have all invested significantly in geothermal projects in recent years. Per Wood Mackenzie, the geothermal sector attracted $1.7B in investment in Q1 of 2025 alone — nearly 85% of 2024’s entire allocation — signaling increased momentum in geothermal production.

Nuclear Fusion

Fusion is the process by which light atomic nuclei, typically isotopes of hydrogen like deuterium and tritium, are combined under immense heat and pressure to form a heavier nucleus, releasing enormous amounts of energy — the same process that powers the sun and stars.

Fusion as a means of energy creation has long been a technically daunting pursuit, requiring decades of intensive research, sophisticated plasma control, and substantial public investment to even approach commercial viability. And yet, in recent years, VCs have started investing in fusion as it has approached commercial viability, largely due to three key advancements: more powerful computer chips, more sophisticated AI-driven simulation, and powerful high-temperature superconducting magnets.

Since the turn of the century, there have been many exciting advancements in fusion research. In 2007, the ITER Organization was established in France to demonstrate fusion energy production’s scientific and technological feasibility. In 2021, the Joint European Torus achieved the first-ever positive yield on a fusion power output. Most notably, in 2022, a U.S. Department of Energy (DOE) lab announced that it had produced a controlled fusion reaction that produced more power than the lasers had imparted to the fuel pellet. The experiment crossed the “scientific breakeven.”

Since this milestone, over a dozen VC-backed startups have each raised $100M+, including Commonwealth Fusion Systems, Helion Energy, Inertia, and Proxima Fusion. In 2025, global private investing in fusion surpassed $10B, including over $2.5B in investment between July 2024 and July 2025. Investors in fusion now include sovereign wealth funds, pension funds, private equity firms, global industrial companies (e.g., Chevron, Shell, and Google), and utilities, reflecting broader institutional and strategic commitment.

AI is also accelerating progress toward commercial fusion energy by transforming critical workflows throughout the fusion lifecycle, such as real-time plasma control, virtual validation environments, predictive diagnostics, and materials discovery. Examples of companies leveraging AI in fusion include the aforementioned Commonwealth, Proxima, and Helion, as well as Thea Energy, Avalanche, and Pacific Fusion.

The willingness of institutional and industrial partners to fund these fusion projects suggests that the prevailing perceived risk in fusion energy has migrated from fundamental scientific viability (“physics risk”) to engineering scale-up and reliable deployment (“deployment risk”). This shift is what gets us excited — fusion is no longer a question of “if” but “when” and “how well.”

A critical data point reinforcing this view is Helion’s power purchase agreement (PPA) with Microsoft. PPAs are typically signed only when end-users have confidence in the commercial delivery of the product, establishing fusion not as an academic exercise, but as a viable technology ready for infrastructure planning. Another positive signal is the U.S. government’s stated focus on fusion. In October 2025, the DOE released its Fusion Science and Technology (FS&T) Roadmap, a national strategy to accelerate the development and commercialization of fusion energy on the most rapid, responsible timeline in history. The Roadmap defines the DOE’s Build-Innovate-Grow strategy to align public investment and private innovation to deliver commercial fusion power to the grid by the mid-2030s.

Achieving commercial fusion would unlock a carbon-free energy source with the potential to reshape global energy systems and accelerate progress towards energy resilience. The pace of innovation is accelerating, bringing this once-distant breakthrough increasingly within reach.

Nuclear Fission

Nuclear fission is a nuclear reaction where the nucleus of a heavy atom, like uranium, splits into two or more smaller nuclei (fission products), releasing a large amount of energy, neutrons, and gamma rays. Within the realm of nuclear, fission offers another promising area of generation that’s carbon-free and capable of supporting AI-scale workloads. The history of fission energy in the United States dates back to the late 1930s and the Manhattan Project. Today, though, many of the country’s nuclear reactors are aging, and new nuclear power plants face intense regulatory scrutiny (12 states currently have some form of restriction on nuclear reactor construction). That said, technological advancements, particularly in the area of Small Modular Reactors, or SMRs, are driving increased investment and enthusiasm in fission energy.

Per Nuclear Business Platform, SMRs offer promise because they can significantly reduce the cost and risk of traditional nuclear fission projects by using standardized designs that can be mass-produced in factories, thereby unlocking predictability and scalability. They can also be sited directly at data centers, circumventing the need for costly grid transmission infrastructure and reducing transmission losses. SMRs are also built with advanced passive safety systems that leverage natural forces such as gravity and convection to prevent accidents without operator intervention.

The efficacy of SMRs is a key factor driving investment in nuclear fission. SMR developers such as X-Energy, NuScale, Kairos Power, The Nuclear Company, and Blue Energy have raised hundreds of millions of dollars in the past year. Overall, nuclear fission investment reached $1.3B in equity funding as of Q3 2025, its highest annual venture funding to date. Similar to fusion, a broad spectrum of institutional investors are now actively investing in fission projects, including VCs, hedge funds, and large enterprises. Google, Amazon, and Microsoft have all recently struck deals with nuclear energy companies, including a PPA between Microsoft and Constellation that could restart the Three Mile Island nuclear power plant in Pennsylvania.

AI is playing a role in optimizing fission operations across predictive maintenance (e.g., identifying equipment failures before they occur), fuel optimization and load forecasting, reactor design, and virtual validation, further increasing the commercial viability of fission energy.

We believe partnerships between would-be customers and utilities, combined with the advancements in reactor development, are de-risking the long-term outlook of nuclear fission, making it a more viable source of energy generation in the medium to long term. In a recent Nuclear Energy Institute survey, 45% of respondents (representing the 95 nuclear reactor facilities in the U.S.) stated interest in partnering with data center operators. The fact that SMRs can be mass-produced and co-located with data centers is particularly compelling — it sidesteps many of the grid bottlenecks that plague other energy sources.

However, no description of fission energy would be complete without mentioning the very real dangers. Accidents at nuclear facilities, while rare, can carry catastrophic and long-lasting consequences for human health and the environment. Radioactive waste from fission is also poisonous to humans and the environment, and difficult to remove. For these reasons and more, fission projects are often subject to lengthy regulatory and permitting processes (e.g., to date, only NuScale’s SMR design has been approved in the U.S.), not to mention supply chain bottlenecks around fuel enrichment and component manufacturing.

We believe meaningful policy reform and safety measures in the U.S. are still needed to unlock the long-term potential of fission energy. One example the U.S. can look to is France, which derives 70% of its electricity from nuclear energy and manages its waste through a closed fuel cycle, significantly reducing the volume of waste needing disposal.

The Future of Power

The energy sources we’ve outlined represent a diverse portfolio of solutions to the AI power bottleneck, each with distinct timelines, risk profiles, and deployment characteristics. Together, they form the foundation of a future energy mix that can support AI’s exponential growth cleanly and scalably.

Our energy thesis is constantly evolving. We started by backing companies at the intersection of energy and compute. As the AI buildout accelerates, we’re increasingly convinced that energy innovation is AI infrastructure innovation. We plan to continue exploring this question and look forward to meeting more founders building at the intersection of power generation and AI who can continue to refine our perspective. If that sounds like you, we’d love to connect. To get in touch, click here.

_

Generating power is only half the equation. To power the AI boom, there must be a dedicated focus on integrating these new sources into the U.S. grid, both physically and digitally. In Part 2 of our energy series, we examine the critical infrastructure challenge facing the U.S.: modernizing an aging power grid built for a different era.